Paluwagan in the Workplace: Helpful or Harmful?

In many Filipino workplaces, paluwagan (a rotating savings system) has been both celebrated and criticized.

As someone who has spent years teaching financial literacy, I’ve seen firsthand how paluwagan can act as both a friend and a foe for employees.

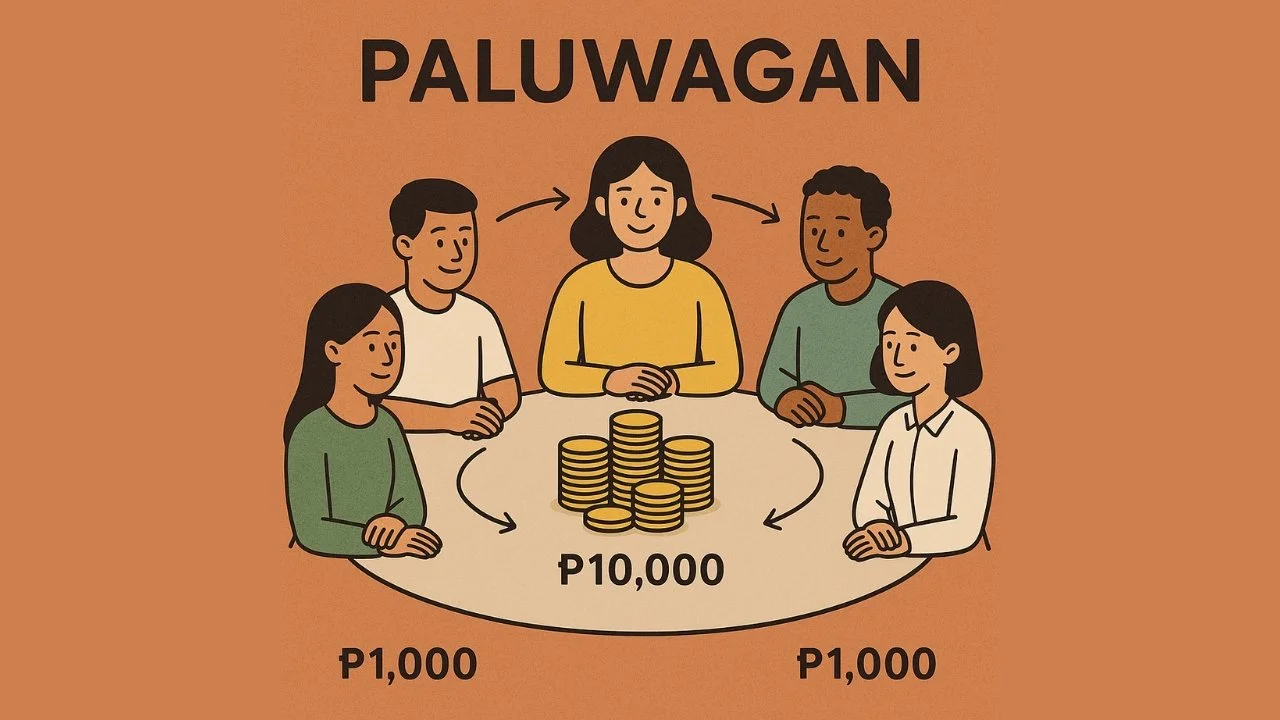

For those unfamiliar, here’s how it works: a group of employees agree to contribute a fixed amount (say ₱1,000 a month). Each month, one member takes the entire pot (₱10,000 if there are 10 members). The cycle continues until everyone has had their turn.

On the surface, it looks simple. But the effects can be mixed.

The Good

When done properly, paluwagan can help employees build discipline because it forces them to set aside money on a regular basis. It also provides access to a lump-sum amount that can be very useful for paying tuition, covering bills, or handling other large expenses. Beyond the money, it also fosters a sense of trust and camaraderie among co-workers, as everyone relies on one another to contribute consistently.

The Not-So-Good

But paluwagan also comes with serious risks. Since it is not backed by any legal protection, members are vulnerable — if someone runs away after getting their share, the entire group suffers. It can also create unnecessary pressure, as some employees may feel forced to join even if their budget can’t really handle it. In some cases, missed or delayed payments lead to tension in the workplace, straining relationships rather than strengthening them. And perhaps most importantly, there is no actual financial growth in paluwagan — money simply moves in circles without earning interest or building wealth.

My Personal Take

I’ll be honest: I’m not in favor of paluwagan as a long-term solution.

It may help with short-term goals, but it should never replace proper financial tools such as:

Emergency savings funds and personal cash reserves

Health and medical insurance

SSS and Pag-IBIG benefits

Proper bank savings and investments (UITFs, Mutual Funds, REITs, stock market, and yes — even Bitcoin HODL)

These tools provide growth, protection, and security in ways a paluwagan simply can’t.

Practical Advice for Employees

If you still want to join a paluwagan:

Keep it small and with people you truly trust.

Set clear rules, deadlines, and penalties.

Use it only as a short-term tool — not your main financial plan.

But if you want to grow your money and secure your financial future, the better path is to:

Build real savings.

Learn to invest.

Protect yourself with insurance.

Final Word

Paluwagan may be a part of Filipino culture, but true financial wellness means going beyond tradition. Don’t just let your money circle around a group — start building habits that let your money work for you.